Planning

Article

Coronavirus cash flow crib sheet

It’s not like cash flow has ever come easy to small and medium-sized businesses. Cash crunch is still by far the number one reason young businesses fail in the UK. But if we already had a cash flow blind spot, coronavirus has brought it into sharp focus. Short-term survival is now directly linked to liquidity.

It’s not like cash flow has ever come easy to small and medium-sized businesses. Cash crunch is still by far the number one reason young businesses fail in the UK. But if we already had a cash flow blind spot, coronavirus has brought it into sharp focus. Short-term survival is now directly linked to liquidity.

Access to government furlough funds, grants or loans might have put out a few short-term fires, but the hard part is still to come. In the conversations we’re having with business owners about their response and recovery plans, cash flow is a recurring concern for the next 12 months. So, in this article, we’ve collected advice and tips and revisited cash flow best practices. Business owners and finance experts believe it’s not too late to work through some of the smart steps.

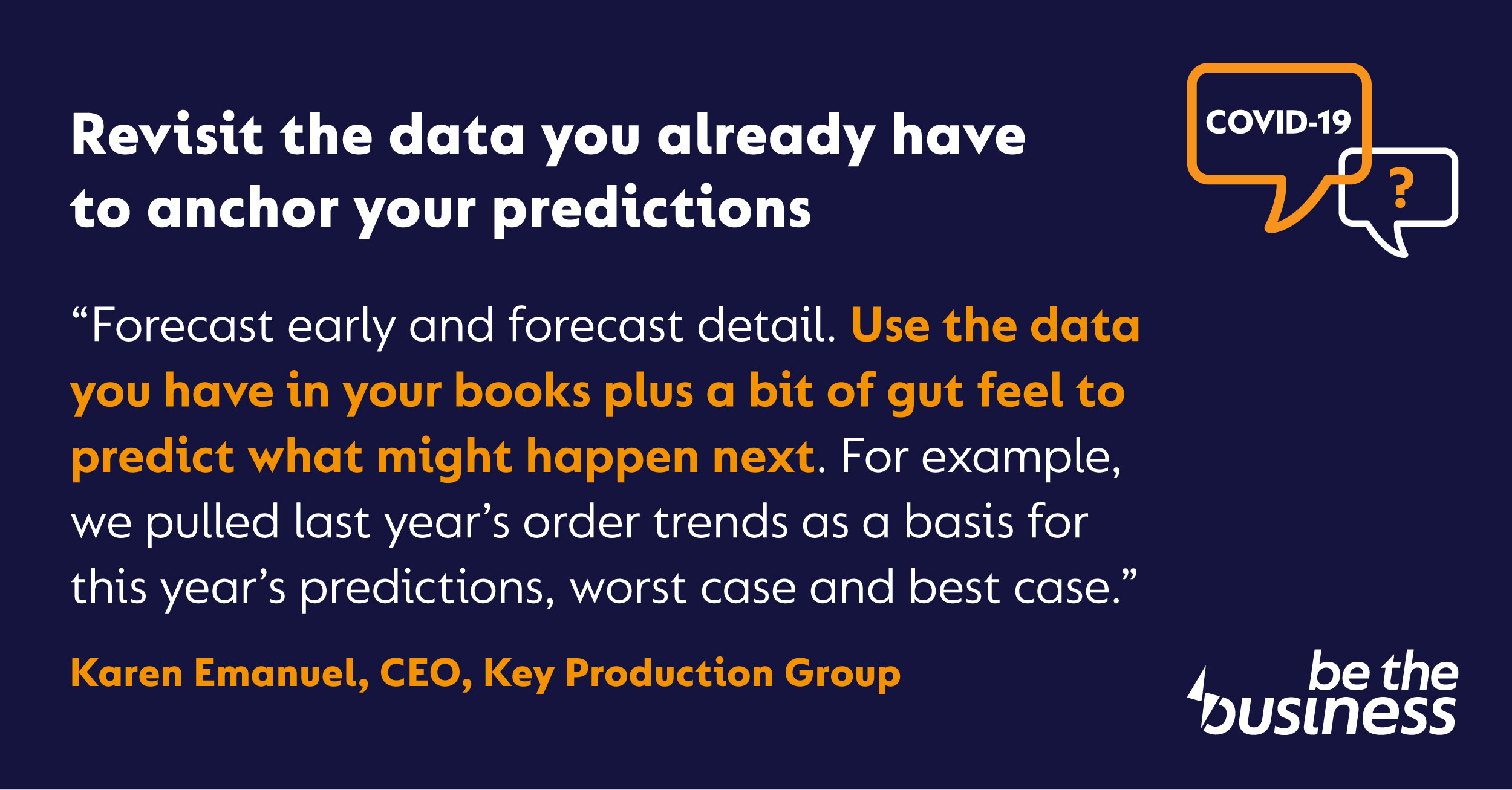

(1) Move to a rolling 12-month forecast

When things are so unpredictable, a rolling cash flow will give you the best estimates of liquidity over the next year and beyond. Rather than look to a single point in the future, such as year-end or Q4, a rolling forecast is always “live” and just keeps extending with each new item you add.

(2) Anticipate big crunch points

Add in key cash flow milestones such as the end of furlough, deferred tax payments coming due, key suppliers going bust, customers withholding payment, a 12-month lull in your order book. Work these events into your outlook, take a view on the likelihood/severity and plan around each situation.

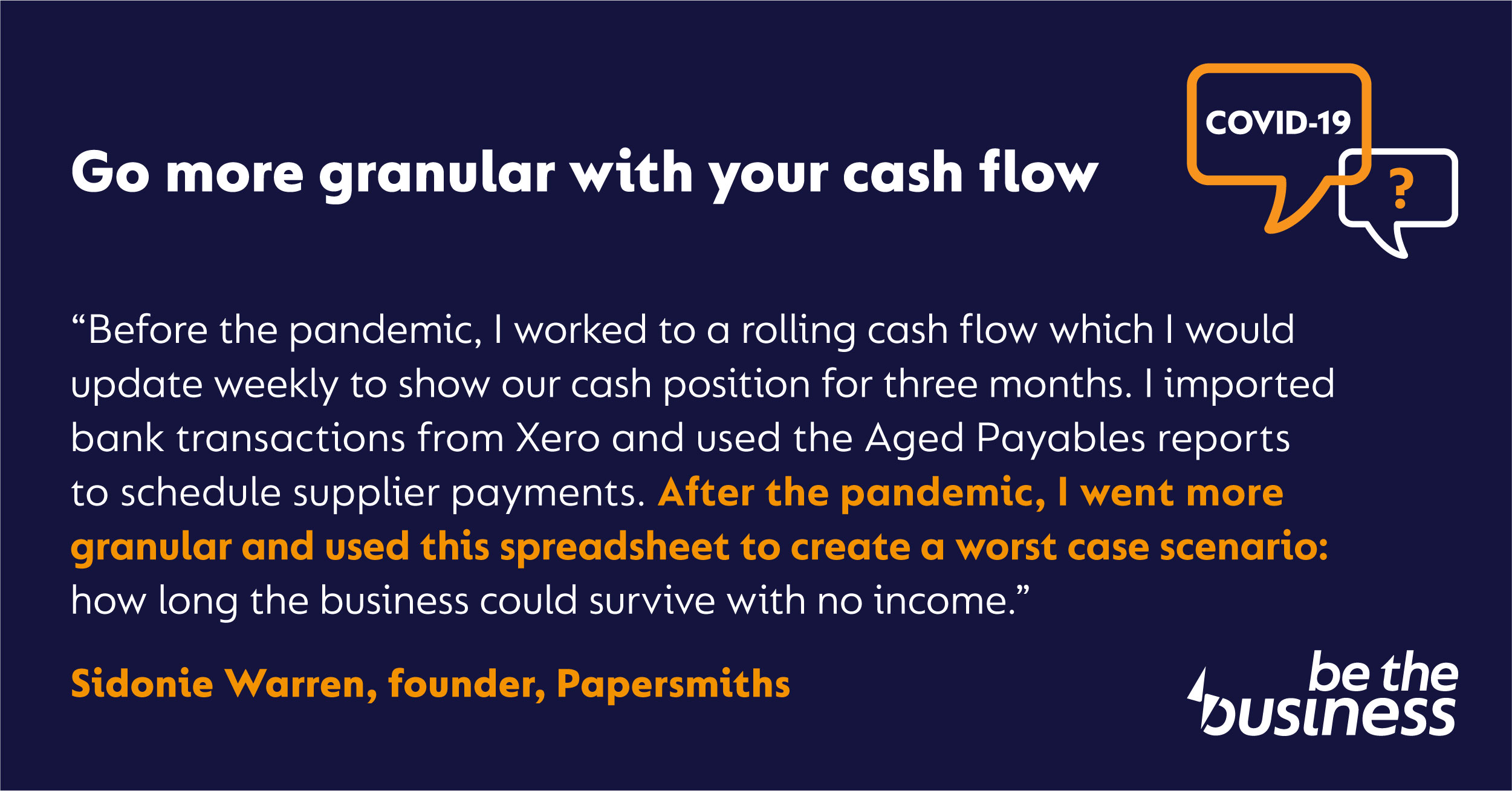

(3) Review cash flow weekly

In normal times, breaking the business numbers down weekly captures most of the granular movements often overlooked in a monthly interval. If you’ve mothballed your business until lockdown ends, weekly might work for a period of inactivity, but many of the businesses we’ve been speaking to are now reviewing cash flow daily. EY has some helpful tips on creating a short-term cash flow forecast.

(4) Sweat the small stuff

When you’re setting up your cash flow forecast, don’t just list the big costs like salary, rent and loan repayments – list them all. Insurance, supplier costs, materials, venue hire, printing, postage, utilities, subscriptions, delivery costs, cleaning, coffee, tea – everything. If you’re sailing close to the wind, those little expenses are what will tip you over the edge.

(5) Pay attention to seasonal variation

If you’re in a seasonal business you don’t need us to tell you there are major cash flow crunch points in your year. Iron out gaps in cash flow by diversifying into new product lines, new customer segments or developing new sales channels. Here are four small businesses that have found ways to keep the cash coming in.

(6) Make it easy to get paid

The aim in good cash flow is to shrink the gap between invoicing and getting paid as much as possible. Cheques are the slowest, online payments are the quickest. Add a payment link to your invoices so that customers can pay using credit card or where possible, switch regular customers to direct debits – here’s a handy how-to guide from Xero.

(7) Make your payment terms crystal clear

Whether you offer 30 days or 15 before an invoice comes overdue, be clear and consistent. Write your payment terms down in your Ts & Cs and highlight them again on each invoice. Add in any consequences for late payment (interest for example) as well as any incentives or discounts for early payment.

(8) Offer retainers to clients

If you’re still billing for hours/days worked, like a consultancy, creative agency or a professional services firm, you probably get a lot of variability in your invoices. This makes it hard to predict your incomings. Even a few monthly retainers can help you avoid an end-of-month scramble for cash. Some useful tips here on how to sell a retainer to your customers.

(9) Have a debt chasing process

As soon as an invoice becomes overdue – day 31 for example – this should trigger the next stage, perhaps a follow-up call. After a second defined period (XX days) this should trigger the next stage – a re-issued invoice for example. Whatever your stages and triggers, be strict about your process. Consider using a collection agency or invoice financing to help.

(10) Stay close to your suppliers and customers

Relationship management is greasing the wheels of your cash flow. Not only is it harder to withhold payment to someone you know, but you can also find manageable payment terms without risking late fees or harming your partnership. Plus, a good understanding of how well they’re doing with cash flow, will give you a more realistic view of yours.

(11) Choose customers and suppliers carefully

Of course, the best way to avoid bad debt is to avoid bad debtors. You might not have the luxury of choice but if you do, credit check suppliers and customers, particularly those that are critical to your business. Check the company’s financial results and credit rating, as well as any CCJs against individuals in those businesses.

(12) Build a fast-paying customer base

If you’re in a position to choose, choose to work more with customers who pay you quickly. They might be smaller projects or bring you slimmer margins, but if cash flow is your priority, profit needs to take a back seat. Invoice deposits if you can and invoice fast – upon completion or delivery, using email to save time and provide you with a record.

(13) Get someone to help

A lot of businesses don’t keep on top of cash flow because it’s another task on the business owner’s to-do list. Take the pressure of yourself by training up someone else in your business to review the day’s credits and debits. It can be your office manager or an admin assistant – they just need to know what indicators to look out for and to when flag them up to you.

(14) Make it easier for yourself

A lot of business owners don’t have a head for figures. If this is you, take the numbers to your management meetings and share or delegate your cash flow forecasting. A spreadsheet will do but of course cloud-based accounting software offers all kinds of benefits such as having a 24/7 overview of all your accounts, data accuracy and back up.

(15) Treat your bank like a customer or supplier

If you’ve applied for the Coronavirus Business Interruption Loan Scheme this month, you’ll know how much data you need to give banks to inspire confidence. As lockdown eases, keep them informed of any unexpected changes in your cash flow forecast. They’ll be more prepared to offer credit and you’ll be in a better position to make a strong application.